The Next Bear Market

According to Wikipedia,

Happy Days Are Here Again is a song copyrighted in 1929 by Milton Anger (music) and Jack Yellen (lyrics). The song was recorded by Leo Reisman and His Orchestra, with Lou Levin, vocal (November, 1929). It was featured in the 1930 film Chasing Rainbows. The song concluded the picture, in what film historian Edwin Bradley described as a “pull-out-all-the-stops Technicolor finale.”

Well, 1930’s Hollywood has come to 21st Century Wall St. and, at the moment, it is certainly “pull out all the stops!” Not only has the Dow hit 25,000, but just about every sector of the market is making new highs: U.S. small and mid-cap stocks, and even overseas developed and emerging markets. About the only laggard has been oil and commodities, and they look like they may have bottomed in the 3rd quarter of 2017 and are now rising sharply. So why am I talking about the next Bear Market?

We believe that we are currently in a Secular Bull Market that still has a number of years to run. (For a definition, see my Blog post of 11/16/17 “Stock and Bond Market Update.”) However, recessions and significant downturns (20+%) do occur within Secular Bull Markets. During the post-war advance that ran from the early 50’s to the late 60’s, there were 3 recessions. Even the great Reagan-Clinton bull market had a recession in 1990. Though we certainly don’t see an imminent recession, there are distant storm clouds forming on the horizon.

Scott Grannis at Calafia Beach Pundit is worried that rising business and consumer confidence, coupled with potential Fed mismanagement of the enormous amount of excess reserves that banks now hold, will lead to higher inflation, higher interest rates and a recession. (See his article here.) He cautions that “none of this is as yet scary or off the charts, but it is worrisome.”

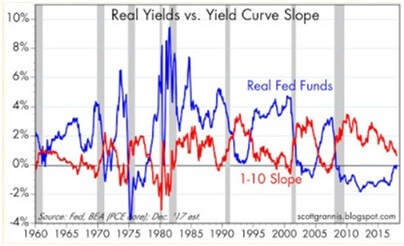

The chart below, which I’ve presented many times before, is my favorite leading recession indicator.

At the moment, the 1-10 slope has not gone negative, and the Real Fed Funds rate has not risen to the 2%+ range that usually precedes a recession. However, the lines are now moving in the wrong direction and closer to downturn territory than at any time since the last recession.

Though a recession may be a few years off, I think it’s wise to make your own personal plans now in a calm, reasoned, dispassionate manner. If you wait to build a storm shelter until the tornado is roaring down your street, you’re likely to panic and make a mess of things.

Your first order of business should be to ask yourself this question: when the signs do point to the likely possibility of a recession, and you make a decision to stay in the market or to get out, where do you want to make your mistake? Do you want to err on the side of caution, or get hurt by being overly aggressive? Leading indicators aren’t foolproof crystal balls; they sometimes give false signals, and even when correct, are often early.

Which of these two scenarios would be more upsetting and damaging to you? You decide to stay in the market, and it declines 20%? Or you go to the sidelines, and the market continues to rise – maybe up 10% over the next 6 months — and you rue the missed opportunity, get back in, and then we get our large decline? Getting out of the market has its own risks.

One final thing to keep in mind: if a recession is on the horizon, the investment “experts” at CNBC and other media outlets will not ring a bell. They will probably downplay the negative yield curve and other indicators that have a decent track record of forecasting recessions. They will talk up the low unemployment rate, high small business confidence and other stats that are either lagging indicators or have a very spotty predictive history. (See my Great Googamooga posts of 12/18/15 and 2/19/16). They will be saying “All is well” like Kevin Bacon at the end of Animal House, but unlike the movie–the truth will not be that obvious.

Now is the time to talk to your Financial Advisor and make plans, not when the rest of the world realizes “all is not well.”

The information contained in this report does not purport to be a complete description of the markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Any opinions are those of Don Harrison and not necessarily those of RJFS or Raymond James. Expressions of opinion are as of this date and are subject to change without notice

Links are being provided for information purposes only. Raymond James is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Raymond James is not responsible for the content of any website or the collection or use of information regarding any website’s users and or members.