Duh!

Back in November, The Washington Post reported that “the White House was thrown on the defensive Wednesday by an inflation report that showed the largest annual increase in prices in three decades, triggering fresh criticisms of President Biden’s legislative plans on Capitol Hill and raising questions about what the administration can do to stem the politically perilous tide of rising prices.”[1]

My thoughts on the White House’s surprise: “Duh! How could you have expected anything else?”

In a talk in India in 1963, the great Milton Friedman said “inflation is always and everywhere a monetary phenomenon.”[2] What did he mean by that? He argued that “one could not find inflation anywhere in the world that was not caused by a prior increase in the supply of money or in the growth rate of the supply of money.”[3]

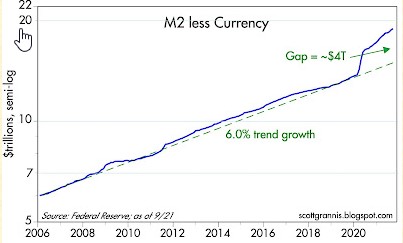

Here is a chart[4] of the U.S. money supply (M2 less Currency), from 2006 through late 2021. As you can see, up until the Federal Reserve and the U.S. government opened the money floodgates with their response to Covid in the spring of 2020, the money supply had basically increased at a 6% annual clip for the previous 19 years. During this time period, the CPI and GNP both grew roughly 2% per year, so a 6% money supply increase is generally consistent with that type of modest inflation and modest economic growth, given that our methods for calculating inflation and economic growth are not absolutely precise.

That all changed in the spring of 2020, when the government began handing out checks, and the Federal Reserve accommodated this largesse by driving down interest rates. The money supply took off like a rocket. Though I don’t have these charts going back to the late ‘60’s and early ‘70’s, when Lyndon Johnson’s “guns and butter” policies fueled an unprecedented U.S. inflation, my guess would be that the rise in the money supply at that time was not as explosive as the current increase.

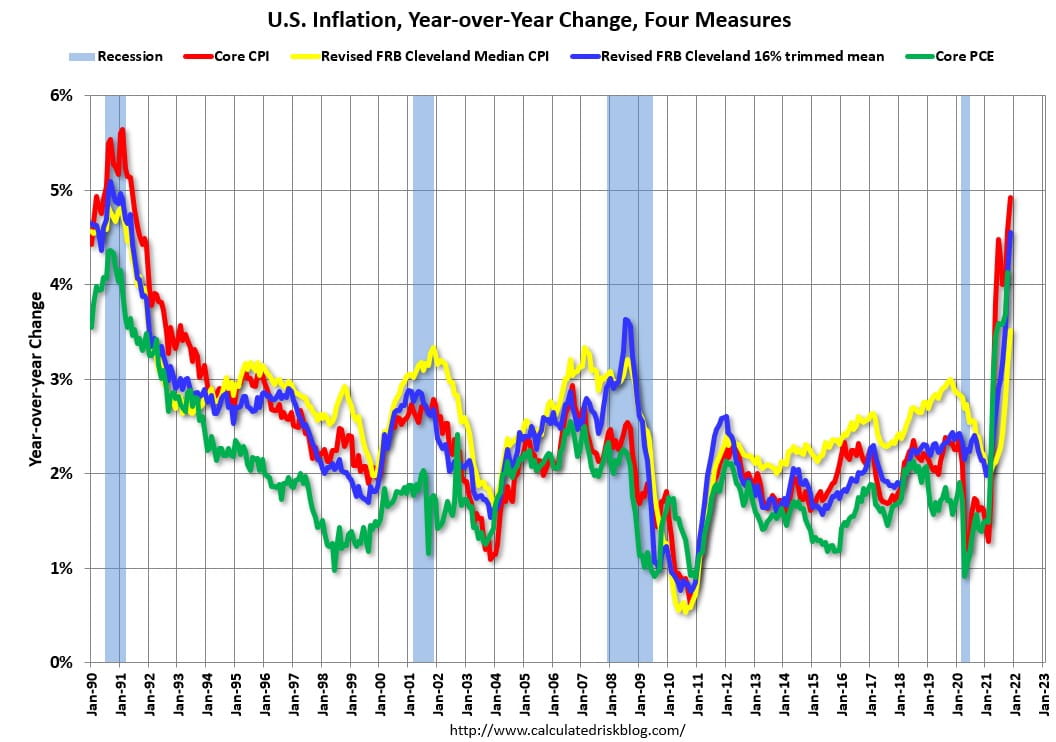

If Friedman’s admonition about inflation is correct, (and I’ve never read anything that convincingly contradicts it), then we could have expected to see inflation jumping in the U.S. after 2020. It took about a year, but that is precisely what has happened, as you can see from the chart below (the CPI is the red line).[5]

Some economists and the government have argued that this is temporary, caused by a number of issues unrelated to the government running the printing press. Brian Deese, Director of the White House’s National Economic Council, thinks that dealing with supply chain issues is the second most important thing the government can do to address inflation, but bizarrely, he believes that getting a Covid vaccine is numero uno.[6] President Biden, as politicians are wont to do, has railed against profiteering oil companies.[7]

To me, these bugaboos (the supply chain issue and oil companies, not the Covid vaccine solution, whose silliness should speak for itself) do not make sense. To understand this, imagine an economy where consumers purchase only two items, fish and clothes. And then imagine that a “supply chain disruption” or “profiteering fishermen” decrease the number of fish available for purchase, thereby driving up the price. Unless the money supply is increased inordinately, this will not lead to inflation, which is defined as an increase in the general level of prices, not just an increase in the price of a single good. Folks will pay more for fish (they have to eat, after all), but they will have less money to spend on clothes, and buy less of them, thereby decreasing demand for clothes and lowering the price. The general level of prices will remain about the same.

I believe the inflation that we are currently experiencing is a direct result of the government’s unprecedented increase in the money supply, and is unlikely to abate any time soon.

Next week: an update on my recession indicators, and a recap of the role inflation has played in previous recessions.

Don Harrison

The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any opinions are those of the author and not necessarily those of Raymond James. Expressions of opinion are as of this date and are subject to change without notice. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Investing involves risk and you may incur a profit or loss regardless of strategy selected. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. Future investment performance cannot be guaranteed, investment yields will fluctuate with market conditions.

[1] The Washington Post, 11/10/21, https://www.washingtonpost.com/us-policy/2021/11/10/inflation-white-house-manchin/

[2] The Hoover Institution, 5/20/21, https://www.hoover.org/research/inflation-true-and-false.

[3] The Hoover Institution, 5/20/21, https://www.hoover.org/research/inflation-true-and-false.

[4] Calafia Beach Pundit, Scott Grannis, 10/27/21, http://scottgrannis.blogspot.com/2021/10/

[5] Calculated Risk blog, https://www.calculatedriskblog.com/search?updated-max=2021-12-10T19:05:00-05:00&max-results=10&start=70&by-date=false

[6] Power Line, https://www.powerlineblog.com/archives/2021/11/inflation-stages-of-disbelief.php

[7] Breitbart, https://www.breitbart.com/politics/2021/11/17/joe-biden-energy-oil-companies-investigation/